Published April 7, 2026

The Conflict in Iran: What It Means for Mortgage Rates and the Housing Market

In the world of real estate, we often say that all economics is local. However, global events have a powerful way of hitting home—literally. As the conflict with Iran continues to dominate the headlines, its ripples are being felt across the U.S. economy, specifically within the mortgage market.

According to a recent New York Times report, the average 30-year fixed-rate mortgage recently climbed to 6.38%, up from 6.22% just a week prior. This marks the highest level we’ve seen since last September, stalling a downward trend where rates had briefly dipped below 6% in late February.

To help our clients and partners navigate these shifts, we’re breaking down the insights of Ruben Gonzalez, Keller Williams’ chief economist, and researcher Isaiah Tabach. Here are the three key ways this conflict impacts your move.

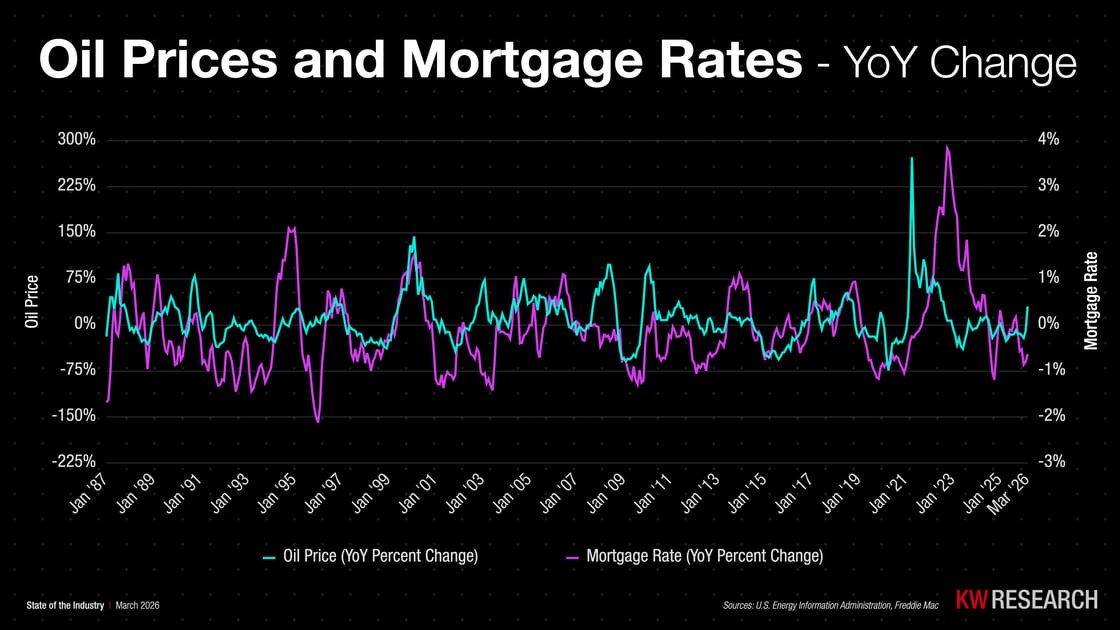

1. The "Supply Shock" Factor

Historically, disruptions in oil supply lead to slower economic growth. We categorize these disruptions into two types:

- Demand Shocks: When the economy grows too fast and everyone wants oil at once (like in 2007-08).

- Supply Shocks: When the oil is there, but it’s "blocked" from reaching the market (like the 1970s).

"Looking at the current situation, it’s clear that what we’re seeing is a supply shock more similar to the ’70s than to 2008," Gonzalez explains. Unlike a demand shock, where prices fall once people stop spending, a supply shock remains until the geopolitical "blockage" is eased. As long as the conflict persists, energy costs remain under pressure.

2. How Oil Drives Mortgage Rates

You might wonder: What does a barrel of crude oil have to do with my home loan? While they aren't directly linked, oil acts as a massive driver of inflation.

Almost every product in your home—from the doorknobs to the drywall—is transported by trucks or ships powered by oil. When fuel costs rise, manufacturers raise their prices to maintain profit margins. This "hidden tax" on goods leads to broad inflation. Because mortgage rates tend to track with inflation and the 10-Year Treasury Yield, higher oil prices almost always exert upward pressure on the cost of borrowing.

3. The Federal Reserve’s Next Move

The Federal Reserve’s primary job is to keep inflation in check. When they see prices rising due to energy shocks, they are less likely to lower the federal funds rate.

Throughout early 2026, the Fed has remained hesitant to cut rates. Fed Chair Jerome Powell recently noted that while they hope this energy crisis is short-lived, a lingering shock may require action to stabilize the economy.

The Bottom Line: There is usually a 2% add-on to mortgage rates above the 10-Year Treasury Yield, and this "spread" often widens during times of global uncertainty.

What Should You Do?

In the short term, mortgage rates are expected to remain relatively stable as the market watches the Fed. However, if the conflict continues to disrupt global oil flow, we could see rates climb further as a tool to curb inflation.

If you are considering a move in 2026:

- Get Pre-Approved Early: Knowing your numbers now helps you pivot if rates shift.

- Watch the Headlines, but Watch Your Budget More: Geopolitics are unpredictable; your personal financial "north star" should be your primary guide.

Questions about how this affects your local neighborhood? Reach out to our team today for a market consultation.